http://answersanswers.com/test/economics/index.html

1. Re-write economics to understate the importance of land rent; roll it in with capital and call the new study “neo-classical economics”. [See chapter and verse of this in Mason Gaffney’s “Neo-classical Economics as a Stratagem against Henry George”.]

1. Re-write economics to understate the importance of land rent; roll it in with capital and call the new study “neo-classical economics”. [See chapter and verse of this in Mason Gaffney’s “Neo-classical Economics as a Stratagem against Henry George”.]

2. Get all economists to claim “There’s not enough natural resource rent to replace tax revenues. It’s only about one per cent of the economy”, without doing the basic mathematics. [Although the claim is patently false*, it is repeated in many economics text books. *Total US land prices have been conservatively assessed at $14.488 trillion. If US GDP in 2012 was $16.245 trillion and land rent is 1%, that means land rent would be about $162.45 billion. But if we divide the land rent by total US land prices, that discloses the overall capitalisation rate, i.e., $162.45 billion divided by $14,488 billion suggests a capitalisation rate of only 1.12%! Sure! Ask any assessor/valuer whether this is even remotely possible!]

3. So, now that we’ve hidden the real quantum of natural resource rent in the economy–at least 25% of GDP–from proper analysis (because it is economists, not land valuers or assessors, who are gifted with the responsibility of ‘running the economy’), the rentier class may then seek to maximise its share of that 25% of the economy. [Remember, although the economic rent of land and natural resources is community-generated, it is predominantly expropriated by the 1%.]

4. Environmental plunder proceeds apace; wealth disparities widen; slowly but surely, financial and social collapse takes hold.

BUSINESS SPECTATOR 31 Jan, 2:19 PM

It’s time to fix Australia’s leaky tax sieve

If the Coalition is serious about addressing our ‘budget emergency’, then it should start with the billions of dollars in foregone revenue that the government fails to collect annually via selective and differential tax policies. Simply slashing expenditure won’t cut it.

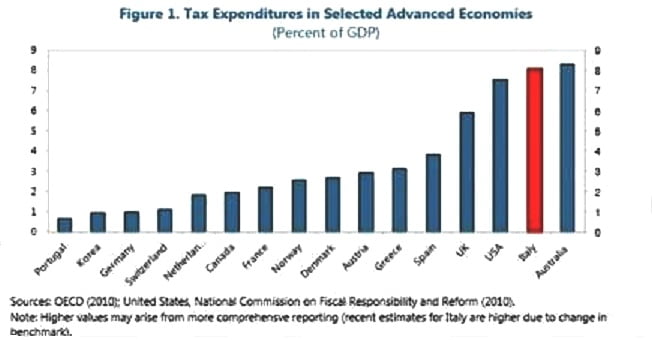

A new report by the International Monetary Fund – on Italy no less – provides important insight into Australia’s tax system. No other advanced country foregoes more tax revenue, through “differential, or preferential, treatment of specific sectors, activities, regions or agents”, on an annual basis than Australia.

This can take the form of selective or differential allowances, exemptions, rate relief, credits and tax deferrals. Australia has seen them all: negative gearing, capital gains taxes and superannuation concessions to name just a few.

These revenues are important since they have “major consequences for the fairness, complexity, efficiency and effectiveness” of the tax system and the broader economy. They change incentives and create opportunities for certain sectors (individuals or organisations) to succeed at the expense of others.

The IMF estimates that this behaviour reduces Australian government revenue by around 8 per cent of GDP. This is more than enough to completely cut the deficit, sharply reduce government debt and leave the budget well placed to handle a declining terms of trade and an ageing population.

Australian governments – of both the left and right persuasion – have proved to be wasteful in recent decades. For the most part, we could afford it. An unprecedented period of prosperity provided ample opportunity for tax cuts, welfare increases and pork barrelling … so much pork barrelling.

We spent money like drunken sailors, feeling smug about our modest surpluses, and then suddenly the money dried up. Tax revenues fell sharply as the global financial crisis began and they have, at best, only mildly improved since then.

The political narrative has been one of reckless spending. But the truth is that our budget deficits are a result of a narrowing tax base and tax cuts that went too far too quickly and without regard for the future.

It was a simple narrative, one with clear lines of blame and appeal to voters, but it missed the complexities of government budgets. It would have been a much tougher sell to blame the population for getting old or for not earning enough or for struggling to find work. It would be a tougher sell still to blame excessive tax cuts.

The Coalition understands this, though it will not admit to it publicly. Look how quickly it wound back its surplus pledge – implicitly recognising the difficulty of running a surplus while dealing with a narrowing tax base and unfavourable demographics.

Now it faces the difficulty of addressing the issue. The evidence so far suggests its members are thinking too narrowly and failing to identify the real issue. The Commission of Audit, set up to identify spending cuts across the government, is a valid endeavour and one worth pursuing but one that is clearly too narrow. The Commission will find a range of spending cuts but that will do little to create a sustainable long-term budget.

If we have a budget emergency – as the Coalition has suggested – then everything should be on the table. Last week I discussed many of the issues that need to be addressed, including winding back negative gearing, cutting superannuation concessions for the wealthy, the aged pension and broadening the tax base via a land tax (Raise taxes to reduce inequality, January 24; A tonic for Australia’s inequality ills, January 27). Those suggestions were made with reference to improving inequality, but they are equality valid approaches to creating a sustainable budget.

Understandably, some people are upset at the prospect of paying more tax. But the truth is we are a relatively low tax-paying country and, as the IMF has shown, there are plenty of ways to avoid paying tax.

Improving our budget balance now – and more importantly, creating a sustainable budget in coming decades – will require hard and often unpopular decisions. But if the Abbott / Hockey government is serious about debt reduction, then it must make those decisions and, in the process, create a long and worthwhile economic legacy.

Why exclude the Goulburn Valley canner, SPC Ardmona, Prime Minister Abbott?

A series of letters in THE AGE today suggests the federal government should be consistent about whom it subsidises. Maybe there’s another side to Treasurer Joe Hockey’s damning indictment of “the entitlement mentality”?

BUSINESS SPECTATOR

Chinese buyers don’t want your house, they want the land

Forget about off-the-plan apartments. What cashed-up overseas Chinese buyers really want is a house in Australia, and more precisely, the land on which the house sits.

For the right house in the right suburb, they are outbidding Australian buyers by $100,000 to $200,000 – and sometimes more – to secure the property. They are importing inflation to their country of choice.

“Many people say, erroneously, that Chinese investors are only buying new-built – I can say categorically that that is not true,” says Andrew Taylor, co-founder of juwai.com, a property website visited by 1.5 million potential Chinese investors each month.

“To most Chinese buyers, re-sales (existing properties) are far more appealing,” says Taylor.

Taylor estimates that Chinese investors spent $5.3 billion buying Australian residential real estate in 2013 – but this is a mere drop compared to the estimated $38 billion to $50 billion they spent buying houses overseas last year.

“The bulk of our enquiries are for established homes, priced at $600,000 to $1.1 million in Australia – the sort of price range most Australians are also targeting.”

One buyer, who didn’t want to give his name, experienced the competition first-hand recently when he looked to buy a home in Epping, a Northern Sydney suburb.

“We saw this house on a Saturday afternoon and when we went to make an offer on the Monday morning, it was already sold – $200,000 more than the asking price ($1 million),” he says.

He subsequently found out that the young Chinese buyer intended to knock it down and spend another $500,000 building a new house on the site.

Veteran Sydney agent Barry Goldman says: “The majority of Chinese buyers prefer to purchase brand new property, or if not new, the property must be substantially renovated or knocked down and rebuilt.

“In Sydney’s leafy mid-north shore suburbs, it is not uncommon to see old houses knocked down and brand new double brick two-storey mansions in their place,” says Goldman, chief executive of Leda Real Estate.

Joseph Ngo, branch manager of LJ Hooker Glen Waverley agent in Melbourne, says it is not unusual for his agency to sell homes in sought-after Melbourne suburbs for $100,000-$200,000 above the expected sale price.

“I recently sold a home for $2.3 million – $500,000 over the asking price,” he says.

“They pay $1.2-$1.3 million for a house and think nothing of tearing it down. Then build a 60-square (557 square metres) mansion on the land. They are buying the land, not the house,” says Ngo.

John McGrath, chief executive of McGrath Estate Agents, says: “We have seen buyer inquiries from clients of Chinese origin (local and overseas) double in the last 12 months.”

Citing figures from the FIRB, McGrath said 9,768 approvals for residential real estate purchases or development were given to foreigners in the 2012 financial year – compared with 4,715 approvals in 2009-2010.

NSW experienced 45 per cent growth – the highest in the nation – in foreign investment in residential real estate.

In total, FIRB recorded residential sales of $4.2 billion to overseas Chinese buyers in the 2012 financial year – up 70 per cent on the $2.4 billion recorded in 2009-10.

Many of these buyers have friends or relatives in Australia to bid for them. Those without the local connections are still able to purchase – and there have been countless anecdotes of overseas Chinese buyers flying in to inspect and buy Australian properties they found on the internet.

According to the FIRB website, foreigners can buy established properties in Australia if they have valid visas – for example, work or student visas. The rationale is that they need somewhere to live, but must sell when the visa expires. While foreigners are otherwise technically not allowed to buy established homes, a Canberra government source said non-resident foreign persons can buy, but they need to apply for approval to buy established dwellings for redevelopment.

Juwai’s Taylor says China’s economic ascendancy has unleashed unprecedented purchasing power for its citizens, and is now washing up on the shores of Australia, the United States, Europe, South America, and Southeast Asia.

“The true power of the Chinese buyer is represented by more than 63 million people whose wealth and incomes provide them with the ability to purchase international property,” says Taylor, who points out that 90 million Chinese search for property online every month. More than 60 per cent pay in cash.

Globally, Taylor says Chinese purchases of residential properties totalled at least $38 billion and possibly as much as $50 billion last year.

And just as they are moving out of tier one cities in China, overseas Chinese investors are now moving out of capital cities, like London, to Manchester and Birmingham.

In Australia, Taylor says, the Chinese are also buying in tier two cities – Gold Coast, Perth and Adelaide. And surprisingly, juwai.com is getting enquiries for properties in Wagga Wagga, in the south west of NSW.

“We didn’t really understand why, until we found out that a Chinese company has made a big investment in Wagga.” (The state-owned Wuai Group has partnered with Sydney-based company ACA Capital Investment to build a $400m trade centre in Wagga.)

The mainland Chinese passion for real estate remained unfulfilled in their home market until about 15 years ago, when private ownership was first permitted, according to Taylor. “They are going through their first property cycle. Property is like gold to them.”

More from Florence Chong

No $25 million bailout for SPC Ardmona.

The Abbott government has rejected providing assistance to the company, although there was cabinet division on the question.

Treasurer Joe Hockey is said to have led the dries, arguing that taxpayers should not bail out SPCA when its parent company Coca-Cola Amatil turned a $215 million profit in the first six months of the current financial year.

The decision was characterised as “a defining point in industry policy”.

No doubt this decision will remain the criterion when Australia’s Big 4 Banks start collapsing when Australia’s bubble-inflated land prices tank. 🙂

Why Things Will End Badly for Investors in US Stocks

by Bill Bonner

Yesterday, we reported on the latest money woes in Argentina. Today, we turn back to the US.

The Dow caught a bid yesterday, with a 90-point rise, bringing it to rest at 15,928.

That’s 15,017 points higher than the low it hit in 1981, just after Ronald Reagan was elected. In 1982, US stocks began a sustained and spectacular rise. Over a 33-year period, the market value of America’s most important corporations rose nearly sixteen-fold.

But wait, did we say ‘value’? We meant price.

Prices are notations, bearing relative information. If you buy a stock at $100 that rises in price another $50…and your brother-in-law’s stock went up to $200, your brother-in-law just got lucky. You wisely bought the more conservative stock and protected your family from the risk. Good on you.

But if consumer prices double…or triple…over the same period, you and your brother-in-law are both chumps.

Of course, it is notoriously difficult to say exactly how much consumer price inflation there is in an economy. Any answer comes with caveats and health warnings.

Argentina’s official inflation number, for example, needs more than the usual boilerplate. Officially clocked at 10% for the last few years, the real annual rate, according to Johns Hopkins professor Steve Hanke, is 63%.

If so, wages, dividends and asset prices all have to be adjusted downward. Based on Hanke’s number, almost all the Argentines are chumps, as almost no asset or income stream can keep pace with the falling value of the peso.

In the US we don’t have to worry about such high inflation rates. We have the Federal Reserve, charged with the mission – among others – of making sure we have a ‘stable currency’.

Back when that job was confided to it, in 1913, there seemed little doubt that it would be up to the task. Consumer prices in the US had been more or less stable since the founding of the Republic.

There had been periods of rising prices – such as the War Between the States – and periods of falling prices – such as the last quarter of the 19th century. But consumer price inflation never developed a real purchase in the US until the Fed was set up to prevent it.

Since then, it has been off to the races.

It would be easy to explain this phenomenon simply as ‘the Fed printed too much money’. But that is not the way it works (at least not these days).

The Fed can add to the monetary base by injecting reserves into the banking system. But this ‘state money’ is only about 15% of what is measured as the wider ‘money supply’…and it doesn’t leave the banking system.

The rest is ‘bank money’. It’s money that is created privately by banks.

These days, banks create this kind of money ex nihilo when they make a loan. If you borrow $100,000 to build a house, for example, a bank simply creates a deposit of $100,000 out of thin air. (The reserve ratios of the financial system these days are so small that they play practically no role at all in constraining credit creation.)

If a bank made 10 loans like this, it would add $1 million to the money supply, which consumers would then spend. Assuming prices are set by supply and demand, this $1 million in new money supply would weigh in on the demand side. Prices would rise, signalling to producers that it is time to increase supply.

Multiply this phenomenon millions of times. Add Alan Greenspan and Ben Bernanke’s ‘party time’ invitations. Mix in the rise of cheap Chinese manufacturing to keep consumer prices and wages down. And don’t forget the bank bailouts…implicit central bank support for stocks…near-zero interest rates…and $4 trillion of QE from the Bernanke Fed.

There you have the potent highball that made so many investors giddy…and brought so much new wealth to the already wealthy.

Fifteen thousand points on the Dow were added in a single generation. More than had been accumulated during the seven generations before.

What made Americans suddenly so smart and so successful?

Or were they?

Stay tuned…

Regards,

Bill Bonner

for The Daily Reckoning Australia

Karl Fitzgerald interviewed German Professor Dirk Loehr on 3CR’s Renegade Economists yesterday. The engaging wide-ranging 30 minute interview touches on Marx, Engels, List, Michael Flurscheim and Silvio Gesell, before moving onto current gentrification pressures in Munich and Berlin and the activist response for land value taxation -> http://www.grundsteuerreform.net/ (Google translate).

See also the English version of Dirk’s Loehr’s Rent-grabbing site.

Experts say Australia’s property bubble is about to burst. Hey! But who are more expert on this question than Georgists, anyway? They also say “Watch out for China!”. That’s also quite correct. Preposterous levels of private rent-seeking in Australia and China, you see?

Once you understand the perils to society and the economy generated by private rent-seeking, you’ll be on top of all this.