A financial critique

The COVID-19 crisis has helped point up flaws in our political economy. The banking industry, share and property markets have undue influence over public policy, with near-impossible levels of private debt leaving many Australians seeking financial relief.

The question of the day is: “What is life going to look like on the other side of the coronavirus?”

It’s evident that we’ve retrogressed over recent years; that a tiny proportion of the population has grown obscenely wealthy as poverty has increased massively. This leads inquisitive souls to consider whether they may have become victims of a distributional system whereby central banks have pumped asset markets, and rent-seeking monopolies permitted to develop, if not encouraged; most obviously in the USA, with Microsoft, Google, Facebook, Amazon, &c.

Worthy objections to financial orthodoxy have been raised. Whilst not suggestive of communism, nor the end days of capitalism, three apparently disparate proposals have emerged from a small band of economists that their erstwhile colleagues have labelled ‘heterodox economics’. They’re not particularly popular.

1. MMT

Encouragingly, it may be that the grim austerity of neoliberal economics— “Where’s the money to come from?”—has had its day, because in dealing with the disastrous socioeconomic effects of the coronavirus, we’ve witnessed that central government spending has been at least partly restorative. In response to neoliberalism’s insistent question, therefore, the money aiding private sector recovery comes from government, from whence expenditures on armaments and warfare are also found, as required.

Private banks had issued America’s currency for decades when the American Civil War broke out in 1861. Abraham Lincoln appointed Salmon Chase his treasurer, and Chase not only financed the war by issuing government bonds, but also by notes of five, ten and twenty dollar denominations, payable on demand. These ‘demand notes’ were effectively union government money. When an alarmed Chase came to Lincoln wanting to know what to do when the cost of the war blew out to between two and three million dollars a day, Lincoln is reported to have breezily volunteered: “Give your paper mill another turn.” A piece purporting to have been written by Lincoln expanding on the idea that government should both print and spend its own currency appears to be of dubious origin. (i.e. https://www.cfoss.com/lincoln.html, cited as Senate Document 23, Page 91, 1865.)

The nonsensical proposition that government deficits represent a blight upon future generations, when they only represent one side of the accounting ledger’s equation, has become so pervasive that Lincoln’s monetary methods—novel by today’s standards—have ironically been tagged “Modern Monetary Theory (MMT) by Australian economist Bill Mitchell.

There’s a distinction needs to be made between central banks issuing money to the financial sector—i.e. the ‘quantitative easing’ that acts to prop up overblown asset markets—and direct government spending into the private sector on welfare and public infrastructure, without borrowing. MMT has obvious advantages over QE, but this isn’t to suggest it doesn’t have its own limitations, especially in connection with inflation.

2. UBI

However, it’s unfortunate that modern monetary theory proponents deem it necessary to affix a Job Guarantee (JG) to the selling of MMT, because a Universal Basic Income (UBI) has a number of more salutary effects than a job guarantee. Whereas the JG appears to be an extension of the gig economy’s blossoming number of underpaid jobs, a UBI not only provides everybody with an income, but also offers people the chance to leave dead-end jobs—including quitting the gig economy—to engage in more productive pursuits. Of all people, one would have expected MMT followers to understand the case for a UBI funded by government, with the implication of distrust in its recipients removed.

In a public address “The Crime of Poverty” on 1 April 1885, the American social philosopher Henry George had an opinion on the matter:

“All prating that is heard from some quarters about its hurting the common people to give them what they do not work for is humbug. The truth is that anything that injures self-respect, degrades, does harm; but if you give it as a right, as something to which every citizen is entitled to, it does not degrade.”

UBIers insist that, far from being an excuse to do nothing, a ‘living wage UBI’ is rather an opportunity to do anything. Were a UBI to be set at a level above existing pensions and subsidies—currently only hard-won after invasive bureaucratic intervention into earnings and privacy—businesses would have to offer potential employees a sufficient wage in addition to their UBI in order to be able to attract them. Exploitative employment that’s “better than nothing”, to which a growing precariat has become accustomed, should not cut it these days as the definition of a fulfilling job.

3. LVT

The idea that taxation constitutes a fund from which government spending occurs has been demolished by MMT supporters. Instead, it represents removal of money from the economy in order to protect the currency from inflation.

Questions arise from this understanding. In deflationary times, exacerbated by the coronavirus, and street riots in France, Hong Kong and the USA, to what extent might taxation actually be reduced to positive effect? And to what extent must taxation be utilised to protect the value of the currency if the government is spending to assist peoples’ welfare? A more obvious question is, to what extent is government inaction currently assisting the wealthy to become wealthier?

Just as it’s passing strange that most MMT people don’t support a UBI, followers of the ideas of Henry George want no taxation at all, yet choose to fly under the banner “Land Value Taxation” (LVT). They do admit to the possibility of ‘sin taxes’ and taxes on polluters; but that’s about it. While they make the point that a ‘tax’ on land values is in the nature of a rent rather than a tax, LVTers would have to convince those believing “the only certainties in life are death and taxes” that the charging of a rent on natural resources is not a tax.

Henry George argued that if ‘unearned’ economic rents flowing from nature itself—which these days include those of the electromagnetic spectrum—are removed from the economy, then labour and capital will receive their rightful reward, unaffected by inflation generated by land prices and the deadweight losses of taxing productivity. This is a more sophisticated argument than of those monetarists who present the idea that inflation is simply the result of “too much money” in the economy. The inquiry may be made of them, on what exactly is “too much money” being spent, if not on land prices and the deadweight losses of taxes on productivity?

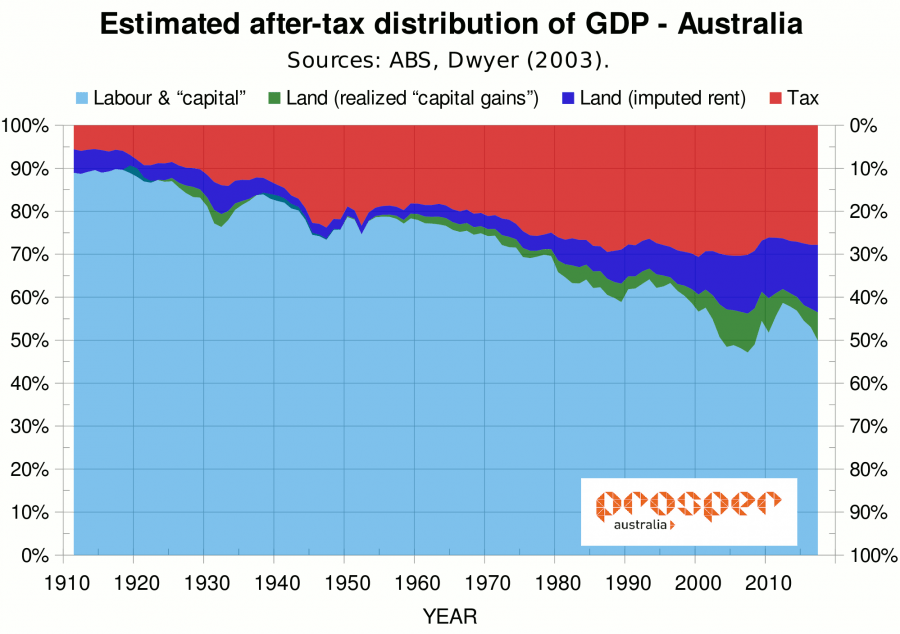

If we accept John Locke’s and Mason Gaffney’s case that all taxes come out of economic rent (ATCOR) in the first instance, Australia’s situation appears to confirm Henry George’s thoughts. Economic rent has grown to account for 50% of the economy, while labour and capital fight tooth and nail over the 50% that is left for them. They’ve not discovered the alternative of working together to remove the counterproductive extractive half of the economy.

Martin Feldstein has shown that income tax injects deadweight losses of up to twice the amount of tax levied into the economy https://scholar.harvard.edu/feldstein/publications/ tax-avoidance-and-deadweight-loss-income-tax, but Australia has stolidly refused to act upon grounded reports such as ‘Australia’s Future Tax System’ (2010), amongst other things, pointing to the benefits taxing of land values which carry no deadweight loss.

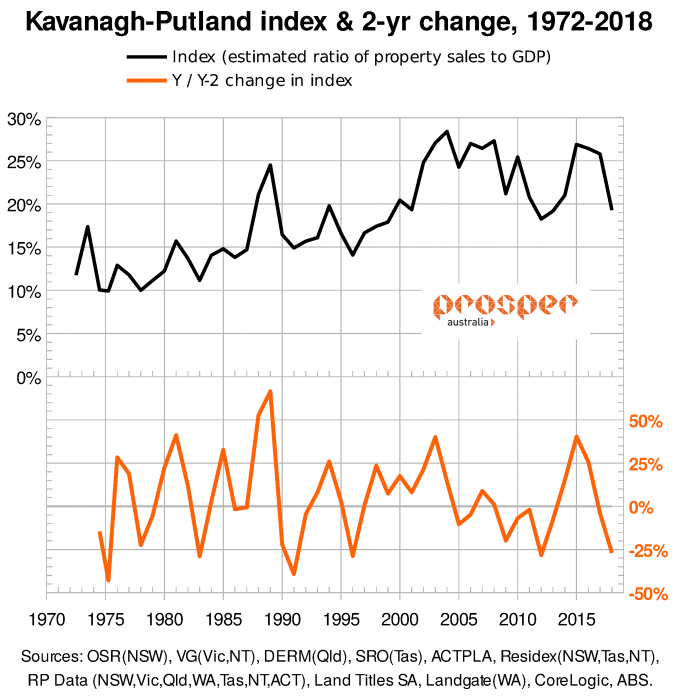

It’s clear then that the tax system actively encourages extractive real estate investment at great cost to national productivity. The case made by Henry George that escalating land prices generate repetitive economic recessions is also borne out by Australian data. Land prices in Australia now comprise an average 70% of property values; therefore volatile land prices play a significant role the following chart of total property prices divided by less-volatile gross domestic product:-

Financial reform is essential if we’re to avoid lurking economic depression. Government and Treasury need to engage urgently with the positive attributes of MMT, UBI and LVT. As these present an opportunity to turn Australia’s invidious financial plight around almost immediately, their consideration is no laughing matter. What would be risible is the crassness of persisting with a financial regime that offers more debt at lower interest rates as an escape from an already impossible level of indebtedness.

MMT and UBI may be considered patches individually, however, bound together with an LVT to assist the ending of inflation, it’s arguable they represent unassailable security for people and the planet.

- Bryan Kavanagh – 28 June 2020