“We have now inflated the current residential bubble to voluminous proportions and economic growth is primed to tank into a major deflation. In the week ended June 3 (2005), Treasurer Peter Costello warned that the Reserve Bank of Australia should not increase interest rates. Early the following week, the RBA seemed to have listened. However, Costello’s advice may have been redundant in the current deflationary environment, because the next adjustment of Australian interest rates would more properly be down.

If we wish to arrest the decline into financial collapse, it may be time for analysts and policymakers to consider to what extent (Sir William) Petty’s national rent offers potential to slash the taxation of productive activity. Replacing taxes with resource rents could also help to keep the lid on skyrocketing land prices, which have played such a destructive role in Australia’s economy during the second half of the fourth Kondratieff wave.”

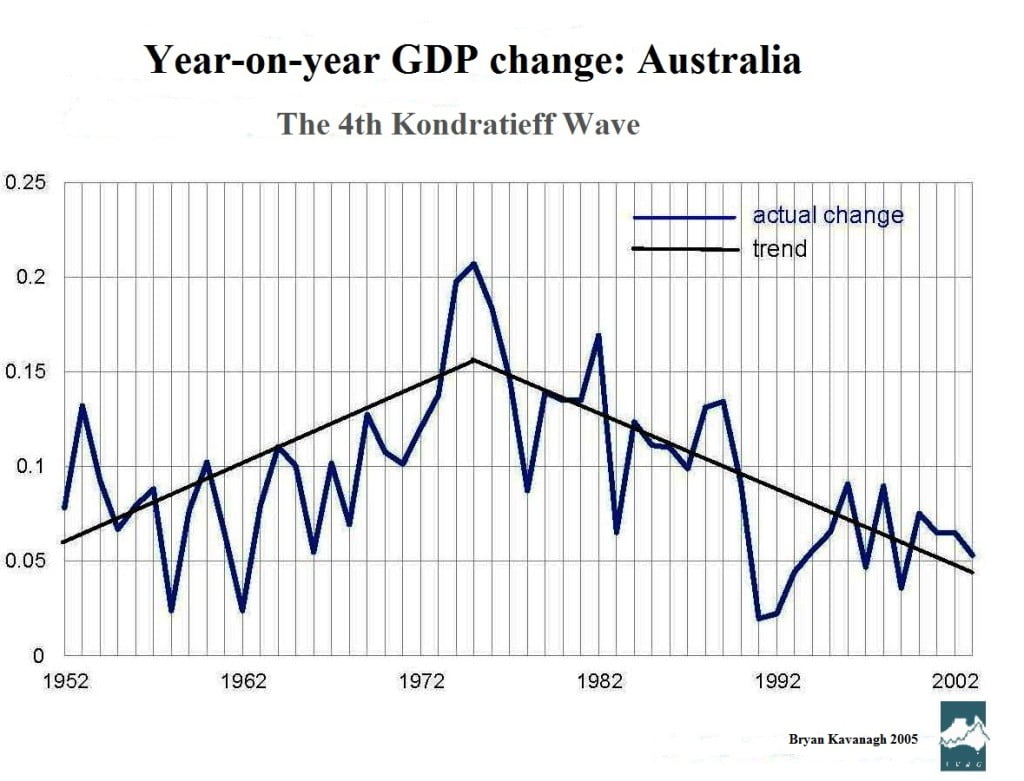

I wrote the above in an article entitled “Resource rents hold the property key” in THE AGE on 15 June 2005 to make the point that the Reserve Bank of Australia’s monthly cash rate announcements are extremely myopic in view of the overarching deflationary environment that ensures interest rates are heading to zero, regardless of what action the RBA takes.

You can either have a property bubble or a rising GDP: you can’t have both.

Some people argue that rates should have gone up in order to take the steam out of the residential market that even then had been in bubble territory for almost ten years in Australia. But I contend that monetary policy is a particularly poor means of achieving such a worthy end, because it also hits those who have borrowed for productive purposes.

The Howard, Rudd, Gillard, Rudd and Abbott governments all had the opportunity to deflate the real estate bubble with fiscal measures that are adequately discriminatory in nature – such as reintroducing a federal land tax, requesting the states to reform and extend their land taxes, abolishing the negative gearing of real estate investment, or requiring local government to be responsible for raising a greater part of its revenue through council rates. But in fear especially of a backlash from the real estate lobby–or maybe of their own real estate investments turning sour?–they chose not to do so, leaving the RBA to carry the can for effective action.

In fact, against the deflationary trend, the RBA did actually increase interest rates from 5.5% to 7.25% from May 2006 to March 2008 pillorying many businesses, before they were overtaken by a dose of reality in the six months to February 2009, slashing the cash rate to 3.25% – down a massive 4%!

We should be alert by now to the fact that a monthly tweaking of interest rates is a very blunt and ineffective instrument that will never replace the good government we’re not receiving, namely, the untaxing of workers and businesses and the capturing of more revenues from land and natural resources.

The Dec 2014 GDP has come in: 2.5% annualised. With a population growth of 1.6%, we’re barely treading water with a GDP growth per capita of 0.9% pa.

If land prices were considered in the inflation rate, interest rates would be much higher.