Rebellions aren’t meant to kick off in lecture theatres – but I saw one last Thursday night. It was small and well-read and it minded its Ps & Qs, and I think I shall remember it for some time.

We’d gathered at Downing College, Cambridge, to discuss the economic crisis, although the quotidian misery of that topic seemed a world away from the honeyed quads and endowment plush of this place.

Equally incongruous were the speakers. The Cambridge economist Victoria Bateman looked as if saturated fat wouldn’t melt in her mouth, yet demolished her colleagues. They’d been stupidly cocky before the crash – remember the 2003 boast from Nobel prizewinner Robert Lucas that the “central problem of depression-prevention has been solved”? – and had learned no lessons since. Yet they remained the seers of choice for prime ministers and presidents. She ended: “If you want to hang anyone for the crisis, hang me – and my fellow economists.”

What followed was angry agreement. On the night before the latest growth figures, no one in this 100-strong hall used the word “recovery” unless it was to be sarcastic. Instead, audience members – middle-aged, smartly dressed and doubtless sizably mortgaged – took it in turn to attack bankers, politicians and, yes, economists. They’d created the mess everyone else was paying for, yet they’d suffered no retribution.

In one of the world’s elite institutions, the elites were taking a pasting – from accountants, entrepreneurs and academics. They knew what they were on about, too. Given his turn on the mic, one biologist said: “I’ll believe economists have reformed when the men behind Black and Scholes [the theory that helps traders value financial derivatives] have been stripped of their Nobel prizes.”

One of the central facts of post-crash Britain is that the elites still hold power, but no longer command the credibility to wield it. You see that when Russell Brand talks on Newsnight about the corrupt lilliputian world of Westminster, and the various YouTube clips total more than 3m views. And I certainly saw it in Cambridge.

Like all the other plebs in Britain – whether on minimum wage, or a five-figure salary – the people in that lecture theatre had been told for decades to trust the politicians, policymakers and employers to provide the jobs, the houses and pensions, and the prospects for their kids. In the wake of the biggest economic rupture since the 1930s, they’re evidently no longer so willing to extend that trust.

But at the same time, the elites – whether in Whitehall or the City – remain in charge. Looking at mainstream economists gives us as good an idea as any as to how reform has been warded off.

As Bateman points out, by rights these PhD-armed boosters of The Great Moderation should have been widely discredited after the crash. After all, the most significant thing to emerge from academic economics in the past five years has not been any piece of research, but the superb documentary Inside Job, in which film-maker Charles Ferguson showed how some of the best minds at American universities had been paid by Big Finance to produce research helping Big Finance.

Yet look around at most of the major economics degree courses and neoclassical economics – that theory that treats humans as walking calculators, all-knowing and always out for themselves, and markets as inevitably returning to stability – remains in charge. Why? In a word: denial. The high priests of economics refuse to recognise the world has changed.

In his new book, Never Let a Serious Crisis Go to Waste, the US economist Philip Mirowski recounts how a colleague at his university was asked by students in spring 2009 to talk about the crisis. The world was apparently collapsing around them, and what better forum to discuss this in than a macroeconomics class. The response? “The students were curtly informed that it wasn’t on the syllabus, and there was nothing about it in the assigned textbook, and the instructor therefore did not wish to diverge from the set lesson plan. And he didn’t.”

Something similar is going on at Manchester University, where as my colleague Phillip Inman reported last week, economics undergraduates are petitioning their tutors for a syllabus that acknowledges there are other ways to view the world than as a series of algebraic problem sets. I was puzzled by this: did that mean Smith, Marx and Malthus weren’t taught? Yes, I was told, by final-year undergraduate Cahal Moran: in development studies. What about Joseph Schumpeter and his theory of creative destruction? Oh, he gets a mention – but literally only a mention.

This isn’t all the tutors’ fault: when you have to lecture to 400 students at once, it’s hard to find time and space to go off-piste. But the result is that economics students come out of exam halls and go off to government departments or the City with exactly the same toolkit that just five years ago produced a massive crash.

Economics ought to be a magpie discipline, taking in philosophy, history and politics. But heterodox approaches have long since been banished from most faculties, claims Tony Lawson. In the 1970s, when he started teaching at Cambridge, the economics faculty still boasted legends such as Nicky Kaldor and Joan Robinson. “There were big debates, and students would study politics, the history of economic thought.” And now? “Nothing. No debates, no politics or history of economic thought and the courses are nearly all maths.”

How do elites remain in charge? If the tale of the economists is any guide, by clearing out the opposition and then blocking their ears to reality. The result is the one we’re all paying for.

______________________

No! It is not time Marx was back on the syllabus. He has had his chance, and made as much of a cock up as capitalism is doing right now. Look around you. The mass of rules and regulation of laws and of people to police it all – that is your Marx. Control, control, and more control. And, while it works for J.P.Morgan, it does not work for the people!

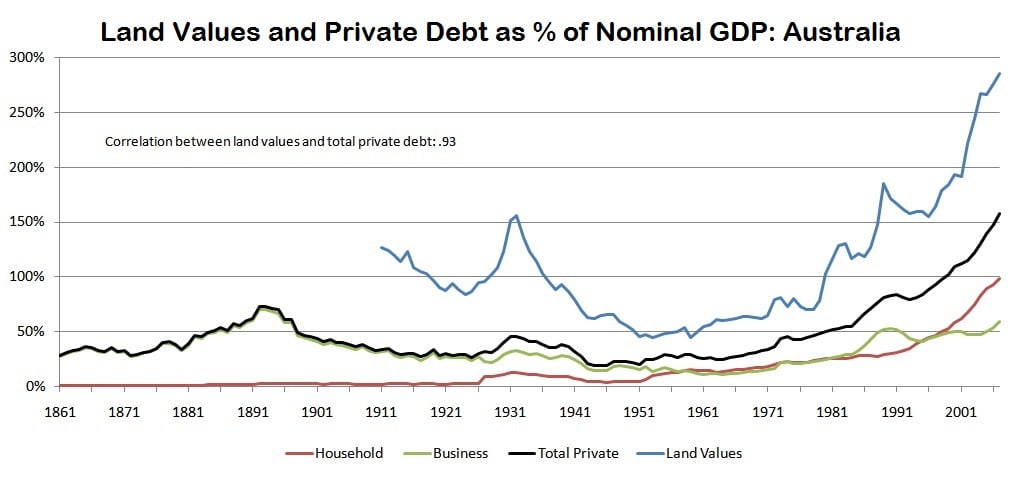

Staring you in the face is the land question. Academics to labourers have advocated the policy of collecting the Ground Rent for over a hundred and thirty years. And the economists’ bosses, the companies and the landowners, don’t want to know, which is why we have political entities (enemies) such as Cameron and Abbott holding the political gun to the nations head.

Reform is desperately needed. A change in thinking is desperately needed.

All wealth is produced by working men. Get used to it. That is not Marxist or Socialist: it is a statement of fact. The place we produce from is called land. And if it is all owned by companies and landowners and governments where does the ordinary man stand? If he pays the ground rent he may get a place to put his bed.

Have you never read “The Great Iniquity” by Leo Tolstoy? The London Times printed it in full, because they thought it was most important. Have you never read “Progress and Poverty” Henry George? Is it too simple to see that there are alternate ideas?

Get out of the working mans pockets, stop taxing his efforts. Freedom is the aim. It starts with the ownership of LAND – you know, the stuff you walk on everyday. It’s worth a fortune, the rent is very high. More so since they stopped making it.

{kind=link}